This article was published in TSE science magazine, TSE Mag. It is part of the Autumn 2025 issue, dedicated to finance and money. Discover the full PDF here and email us for a printed copy or your feedback on the mag, there.

The greatest financial revolution may not be on Wall Street – but in rural Kenya, Brazil’s shopping malls and Peruvian markets. We asked a TSE development economist how digital innovation is changing the way people use money in the Global South.

Why is mobile money so transformative?

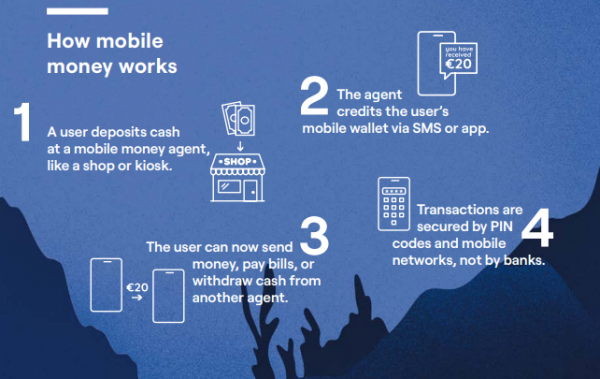

It’s about access. In many countries, banking services don’t reach rural areas or poor households. Mobile money lets users store and transfer funds by mobile phone, without using a traditional bank account.

Economists have shown that mobile money boosts financial inclusion and allows faster, cheaper remittances. This can lift people out of poverty, support small businesses, reduce gender inequality, and help families to survive crop failure, drought, and medical emergencies.

What’s the secret of success?

There’s no one-size-fits-all model, but our study of four leading payment systems identified several key ingredients:

- Digital design – Is the system easy to use? Are fees affordable?

- Smart regulation – Is there a legal framework that balances innovation with oversight?

- Interoperability – Can users transfer money between platforms and banks?

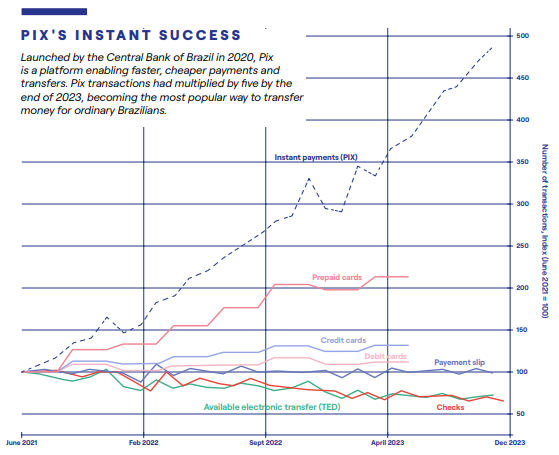

Brazil’s Pix succeeded by combining public leadership with interoperability. Kenya’s M-Pesa, by contrast, was a private initiative that grew fast in a lightly regulated space. Both worked, but for different reasons.

How is mobile money likely to evolve?

Mobile services are expanding to include credit, insurance, and even investment products. In some places, mobile finance may leapfrog traditional banking. This raises the bar for regulators to ensure digital infrastructure is equitable and secure.