What happens when governments attempt to curb consumption of sugary drinks and other unhealthy products? In a new study, TSE Health Center Director Pierre Dubois and his coauthors (Rossi Abi-Rafeh, Rachel Griffith, Martin O’Connell) evaluate the impact of sugar taxes and advertising restrictions in the UK. By accounting for firms’ strategic responses, their innovative framework has the potential to advance research on public health policies in a wide range of other markets and contexts.

What are sin taxes? How much do we know about their impact on firms?

Sin goods include products such as tobacco, alcohol, and high-sugar food and beverages, whose consumption is linked to negative health effects. They may produce internalities if people partially ignore privately borne health costs; or externalities if costs are borne by others, for instance, through public health care or health insurance premiums. Many governments are now imposing taxes and advertising restrictions in an attempt to reduce consumption of sin goods.

These policies are likely to impact corporate strategies, as firms adjust their prices and advertising expenditures in response. As advertising can affect product demands over time, the introduction of sin taxes can have dynamic effects on the market equilibrium. However, there is little work that studies the interactions of taxes and advertising restrictions, or that accounts for the possibility that firms reoptimize advertising expenditures in response.

Why is the UK cola market an interesting case study?

Taxes that aim to reduce consumption of sugary drinks, due to their association with obesity and diet-related disease, have been implemented in the UK and more than 50 jurisdictions. Firms can avoid the UK tax by lowering the sugar content of their products. Only Coca Cola, Pepsi, and a few niche energy drinks pay the tax. This allows us to capture the majority of products subject to the tax.

Sweetened beverages are highly advertised in the UK, accounting for 4% of consumer spending on food and drinks but 7% of television advertising. Two-thirds of advertising for sweetened beverages was for cola products. Coca Cola and Pepsi dominate, while lower quality, store-brand alternatives are not advertised. We focus on TV ads, which constitute the bulk of advertising in the cola market.

How do you account for strategic responses to sin policies?

Firms’ advertising strategies are potentially complicated high-dimensional objects, involving choices over the timing and placement of each advert. This requires consideration of advertising prices, expectations about viewing behavior, and the impact on future demand. In the UK, however, Coca Cola and PepsiCo delegate the task of choosing specific slots to an advertising agency. This intermediary role for agencies, which is common in other markets, simplifies our analytical challenge by reducing firms’ action space to a more straightforward decision over total monthly expenditure on advertising.

As with advertising levels, firms’ decisions over product prices depend on the sensitivity of consumer demand. We combine rich longitudinal micro data on UK household purchases with detailed information on viewing habits and TV advertising. To identify the impact of advertising exposure on demand we exploit variation in advertising across households with the same demographic make-up and viewing habits. We can then simulate the impact of different policies on firms’ optimal pricing and advertising budgets.

What are your key findings?

Our demand estimates show brand advertising creates positive spillovers. For instance, Regular Coke advertising does not just raise demand for Regular Coke, it also stimulates demand for Diet Coke and (to a lesser extent) Pepsi. These spillovers play an important role in driving advertising responses.

Our results also suggest that firms respond to a sugar tax by reducing advertising of taxed products. A key reason is our finding that price-sensitive consumers tend to be more advertising-sensitive. This means that the tax drives advertising-sensitive consumers away from taxed brands, lowering firms’ incentive to advertise. The reverse could happen if consumers’ sensitivity to advertising is unrelated to their price sensitivity. The reduction in advertising is larger when the tax is a percentage of price (ad valorem) rather than a specific tax per unit volume. This is because the ad valorem tax reduces optimal price-cost margins, reducing the profitability of the marginal consumer.

Both a sugar tax and advertising restriction lead to reduced advertising of diet brands. This is partly driven by the positive spillovers that create within-firm complementarity in advertising strategies. For firms, the lower the advertising of sugary products, the lower the return to advertising diet products.

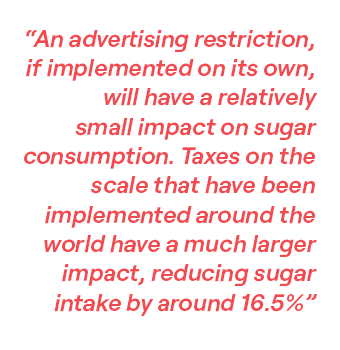

Overall, our results suggest that an advertising restriction, if implemented on its own, will have a relatively small impact on sugar consumption (-2.7%). Taxes on the scale that have been implemented around the world have a much larger impact, reducing sugar intake by around 16.5%. The impact of an advertising restriction is substantially reduced if combined with an existing tax that may have already driven away susceptible consumers.

Do these sugar taxes unfairly penalize poorer consumers?

The taxes may appear regressive, as low-income households suffer more from higher prices. However, their loss is offset by larger sugar reductions. Based on the estimates of Allcott et al. (2019), the reduction in negative health outcomes and other internalities achieved by the tax is broadly enough to compensate consumers in each income quartile for the impact of higher prices.

FURTHER READING Pierre’s publications including ‘The Effects of Sin Taxes and Advertising Restrictions in a Dynamic Equilibrium’ (2024), ‘How well targeted are soda taxes?’ (2020) and ‘The effects of banning advertising in junk food markets’ (2018) are coauthored by Rachel Griffith and Martin O’Connell and available to view on the TSE website. For other TSE studies on sin taxes, see Bonnet and Réquillart (2013).

Article published in TSE Reflect, April 2024